TL;DR:

- Standard carrier liability does not fully protect against common international shipping risks.

- Choosing the right insurance policy depends on cargo value, route risk, and product fragility.

- Proper compliance and documentation are essential for valid claims and avoiding coverage denial.

Many Pennsylvania businesses shipping internationally assume their goods are fully protected the moment a carrier takes possession. That assumption is costly. Standard carrier liability covers only a fraction of actual cargo value, and the fine print excludes a long list of real-world risks. Whether you export manufactured goods through Philadelphia or import raw materials via Pittsburgh, the exposure is real and often underestimated. This guide breaks down how international cargo insurance works, which policy types suit your shipping profile, how the claims process unfolds, and what compliance factors Pennsylvania businesses must track to avoid denied claims.

Table of Contents

- Why international cargo insurance matters for Pennsylvania businesses

- Key types of international cargo insurance explained

- How the insurance process works: from quote to claim

- Compliance factors unique to Pennsylvania and international shipments

- A smarter cargo insurance strategy: what most businesses overlook

- Unlock comprehensive cargo coverage for your international trade

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Coverage gaps exist | Standard carrier liability rarely covers the full value or range of risks for international shipments. |

| Policy types matter | Choosing the right cargo insurance type can save your Pennsylvania business from costly losses. |

| Process is manageable | Securing and claiming cargo insurance is straightforward with the right documents and partners. |

| Local compliance is critical | Pennsylvania businesses must ensure both U.S. and destination country compliance for claims to succeed. |

| Expert guidance helps | Working with experienced providers can spot coverage gaps and streamline the insurance process. |

Why international cargo insurance matters for Pennsylvania businesses

With our foundation set, let’s examine the risks and why your business may be more vulnerable than you think.

Pennsylvania sits at a strategic crossroads for U.S. international trade. The state’s manufacturers, distributors, and importers move billions of dollars in goods annually through ocean, air, and intermodal channels. Yet many of these businesses operate under a dangerous misconception: that the carrier is responsible for everything that goes wrong in transit.

The reality is far more sobering. Standard carrier liability does not cover full cargo value or all risks. Ocean carriers, for instance, typically limit liability to $500 per shipping unit under the Carriage of Goods by Sea Act, regardless of what the cargo is actually worth. Air carriers follow similar limitations under the Montreal Convention. That gap between what a carrier pays and what your goods are actually worth can be financially devastating.

Common loss scenarios that businesses encounter include:

- Storm damage during ocean transit, particularly on Atlantic routes

- Port accidents involving mishandling of containers during loading or discharge

- Theft at foreign ports or during inland transport legs

- Contamination from co-loaded cargo or improper storage conditions

- General average declarations, where all cargo owners share the cost of a maritime emergency even if their goods were undamaged

Business size does not reduce exposure. A small Pennsylvania exporter shipping $80,000 in specialty equipment faces the same carrier liability ceiling as a large corporation. The difference is that a large company may absorb the loss; a small one may not.

This is precisely where freight forwarding in Pennsylvania intersects with insurance planning. A knowledgeable freight partner helps identify coverage gaps before shipment, not after a loss occurs.

“The question is never whether a loss can happen. The question is whether your business can survive it without proper coverage in place.”

Experts who study best transport business insurances consistently find that underinsurance is the leading cause of financial hardship after cargo incidents. Understanding cargo insurance basics is the first step toward closing that gap.

Key types of international cargo insurance explained

Understanding the ‘why’ lets us dig deeper into ‘how’: What are your options, and which actually protect your shipments?

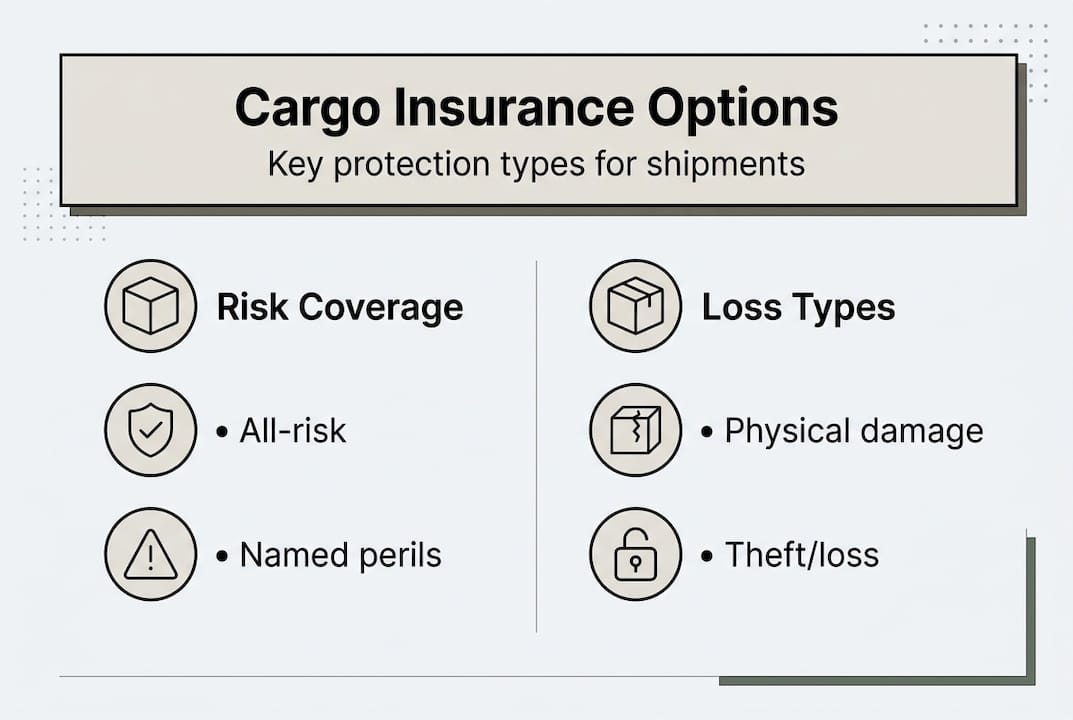

Different policies cover different risk profiles and loss types, so choosing the wrong one is almost as bad as having no coverage at all. The three primary policy structures are all-risk, named-peril, and total loss only.

| Policy type | What it covers | Best for |

|---|---|---|

| All-risk | Most causes of loss unless specifically excluded | High-value or fragile goods |

| Named-peril | Only the specific risks listed in the policy | Durable, lower-value cargo |

| Total loss only | Covers only complete destruction or loss of entire shipment | Bulk commodities |

Here is how Pennsylvania businesses typically navigate these options:

- Assess shipment value. High-value electronics, pharmaceuticals, or precision machinery almost always warrant all-risk coverage.

- Evaluate route risk. Shipments transiting regions with elevated theft or political instability benefit from broader protection.

- Review product vulnerability. Fragile or perishable goods need policies that address damage, not just total loss.

- Compare exclusions side by side. Two all-risk policies can differ significantly in what they exclude.

- Match policy duration to transit time. Warehouse-to-warehouse coverage is broader than port-to-port.

Pro Tip: Never evaluate a cargo insurance policy by its name alone. The exclusions section is where the real story lives. A policy labeled “all-risk” may still exclude inherent vice, delay, or improper packing, all of which are common causes of loss.

Businesses exploring import cargo insurance types will find that all-risk policies dominate for high-value international shipments, while named-peril options serve businesses with tighter margins on lower-value goods. Reviewing freight insurance options alongside your freight partner gives you a clearer picture of what the market offers.

Studies on examples of business risks in transport confirm that businesses that proactively match policy type to cargo profile file significantly fewer disputed claims.

How the insurance process works: from quote to claim

Now that you know what to look for, let’s break down how the actual insurance journey unfolds.

Securing cargo insurance does not have to be complicated. A straightforward process minimizes shipment disruptions and keeps your supply chain moving. Here is the step-by-step flow:

- Request a quote. Provide cargo value, commodity type, origin, destination, and transit mode.

- Submit shipment details. Include packing method, container type, and any special handling requirements.

- Review and finalize the policy. Confirm coverage scope, exclusions, and the insured value before signing.

- Arrange payment and receive the certificate. The insurance certificate must travel with shipping documents.

- File a claim if loss occurs. Notify the insurer immediately, document the damage, and submit required paperwork.

| Cost driver | Impact on premium |

|---|---|

| Cargo value | Higher value increases premium |

| Destination risk | High-risk routes increase cost |

| Commodity type | Fragile or high-theft goods cost more |

| Coverage scope | All-risk is more expensive than named-peril |

| Transit mode | Ocean typically costs less than air per value |

Claims for international shipments are assessed based on the survey report from an independent marine surveyor, the original invoice value, and the bill of lading. Most straightforward claims resolve within 30 to 60 days, though complex cases involving third-party liability can take longer.

Pro Tip: Maintain a complete documentation file for every shipment, including photos of cargo before loading, packing lists, and commercial invoices. Insurers assess claims based on evidence, and gaps in documentation are the single most common reason for delayed or reduced payouts.

Reviewing cargo insurance coverage options before your next shipment departs is far easier than reconstructing records after a loss. Businesses new to the process will also benefit from reviewing international shipping basics to understand how documentation flows across the entire transit chain. Checklists similar to a warehouse safety checklist applied to cargo documentation can dramatically reduce claim friction.

Compliance factors unique to Pennsylvania and international shipments

A solid insurance policy only pays off if you meet all the legal requirements. Here is what sets Pennsylvania apart.

Insurance coverage does not exist in a vacuum. Compliance affects eligibility for coverage and claim success, and Pennsylvania businesses face a layered set of federal, state, and international requirements that directly influence whether a claim will be honored.

Key compliance checkpoints include:

- Export Control Classification Numbers (ECCNs): Goods subject to export controls must be properly classified. Misclassification can void coverage.

- Customs documentation accuracy: Errors on commercial invoices, packing lists, or certificates of origin can trigger claim denials.

- Incoterms selection: The chosen Incoterm (such as CIF or FOB) determines who is responsible for insurance at each leg of the journey.

- Sanctions screening: Shipping to sanctioned destinations or parties invalidates insurance coverage entirely.

- Pennsylvania-specific licensing: Certain commodities require state-level export licenses in addition to federal clearances.

Non-compliance does not just create legal risk. It creates a direct financial risk by giving insurers grounds to deny claims that would otherwise be valid. Businesses that invest in customs compliance tips before shipment departure dramatically reduce their exposure on both the regulatory and insurance fronts.

Statistic callout: Industry data shows that cargo claims involving documentation errors or compliance violations are denied at rates significantly higher than claims with complete, accurate paperwork. The margin is not small. It can be the difference between a full payout and zero recovery.

Understanding container shipping basics also matters here. Container-specific requirements, including seal integrity, weight declarations, and verified gross mass compliance, all affect both customs clearance and insurance validity. A single missed requirement can unravel an otherwise solid policy.

A smarter cargo insurance strategy: what most businesses overlook

Most articles on cargo insurance stop at policy types and claims steps. But the businesses that consistently protect their margins do something different. They treat cargo insurance as a living part of their logistics strategy, not a checkbox completed once a year at renewal.

One of the most overlooked risks is underinsurance. Many Pennsylvania businesses insure cargo at invoice value but forget to include freight costs, duties, and the expected profit margin, meaning even a full payout leaves them short. The standard practice in marine insurance is to insure at 110% of CIF value (cost, insurance, and freight) to account for these hidden losses.

Another gap involves policy stacking confusion. Some businesses assume that a freight broker’s policy and their own policy provide double coverage. In practice, both policies may contain clauses that make each one secondary to the other, leaving neither fully active.

Reviewing actual claims data, not just sales materials, is how experienced shippers identify these gaps. Ask your insurer for anonymized examples of denied claims in your commodity category. That data is more useful than any brochure.

Businesses that master international freight shipping understand that the policy is only as strong as the process behind it. Annual policy reviews, post-claim audits, and proactive compliance checks are what separate businesses that recover quickly from those that absorb losses silently.

Unlock comprehensive cargo coverage for your international trade

Ready to transform your approach and shield your business? See how our solutions make cargo insurance simple.

Worldwide Express, Inc. offers Pennsylvania businesses a single platform for managing international cargo risk from quote to claim. Whether you need guidance on cargo insurance solutions, want to explore your options through a detailed freight forwarding guide, or need to compare freight insurance options, the resources are ready when you are.

Our team brings deep expertise in customs compliance, documentation, and global carrier networks so that your coverage actually holds up when it matters. From first shipment to full supply chain management, Worldwide Express is built to help you move goods confidently across borders. Reach out today to request a freight quote or explore the full range of cargo protection tools available to your business.

Frequently asked questions

What does international cargo insurance cover?

International cargo insurance typically covers loss, damage, and theft for insured shipments, including events like storms, port accidents, and mishandling that standard carrier liability does not address.

Is cargo insurance mandatory for shipments from Pennsylvania?

Cargo insurance is not legally mandatory, but most shippers recommend it strongly because carrier liability limits leave significant gaps in financial protection for international shipments.

How much does international cargo insurance cost?

Insurance cost is linked to cargo value, destination risk, and coverage type, but it typically represents a small percentage of the total shipment value, making it one of the most cost-effective risk management tools available.

Can I add cargo insurance after my shipment has left Pennsylvania?

Insurance is binding before shipment departs, so arranging coverage after goods are already in transit is rarely possible and, when available, comes at significantly higher cost with limited scope.